Important Disclaimers

Before reading and deploying this strategy, please pay attention to the following three points:

1. The strategy requires patience before it opens its first position

Binance perpetual delistings are low-frequency events — they don’t happen every day. After launching the strategy, you may need to wait several days, or even longer, before the first position is opened. The program spends most of its runtime in a “standby monitoring” state. Be mentally prepared for long idle periods, and don’t assume the strategy has failed just because there has been no trading activity in the short term.

2. There is still room to optimize the detection timing

This article uses a scheme that polls the fapi/v1/exchangeInfo endpoint every 15 seconds and identifies delisting signals via changes in the deliveryDate field. Live testing shows this method has some latency and is not the fastest path. Readers can further optimize the detection mechanism based on their own needs — for example: shorten the polling interval, monitor Binance’s announcement API in parallel, subscribe to WebSocket pushes, or cross-validate using multiple signal sources. The earlier you enter, the more of the first sharp drop you can capture.

3. Shut the strategy down in time to prevent profit giveback

Live observation shows that not every delisted token grinds down all the way to the delisting moment. Some tokens drop sharply right after the announcement and then gradually rebound over several hours to a full day, sometimes recovering back to pre-announcement levels. If you don’t shut the strategy down in time, the floating profits accumulated earlier will be heavily eaten into by the rebound — and can even flip from gain to loss.

It is recommended to set any of the following as an active exit signal:

- Liquidate immediately once a preset profit target is reached;

- Force-close when the price rebounds beyond a certain percentage (e.g., 20%–30%) above the post-announcement low;

- Trigger a profit-protection close when drawdown from peak P&L reaches a certain percentage (e.g., 30%–50%).

Do not passively wait for the T-60-minute force-close — that is a safety net, not an optimal exit.

Introduction

In Binance’s perpetual market, there is a special type of opportunity that most people overlook — contract delisting events.

From time to time, Binance issues announcements declaring that certain illiquid or low-volume perpetual contracts will be delisted. The instant the announcement drops, the market reacts swiftly: long holders are forced to close out, panic selling cascades in, and the price typically plunges within minutes. After that comes a long, choppy downtrend that lasts all the way to delisting.

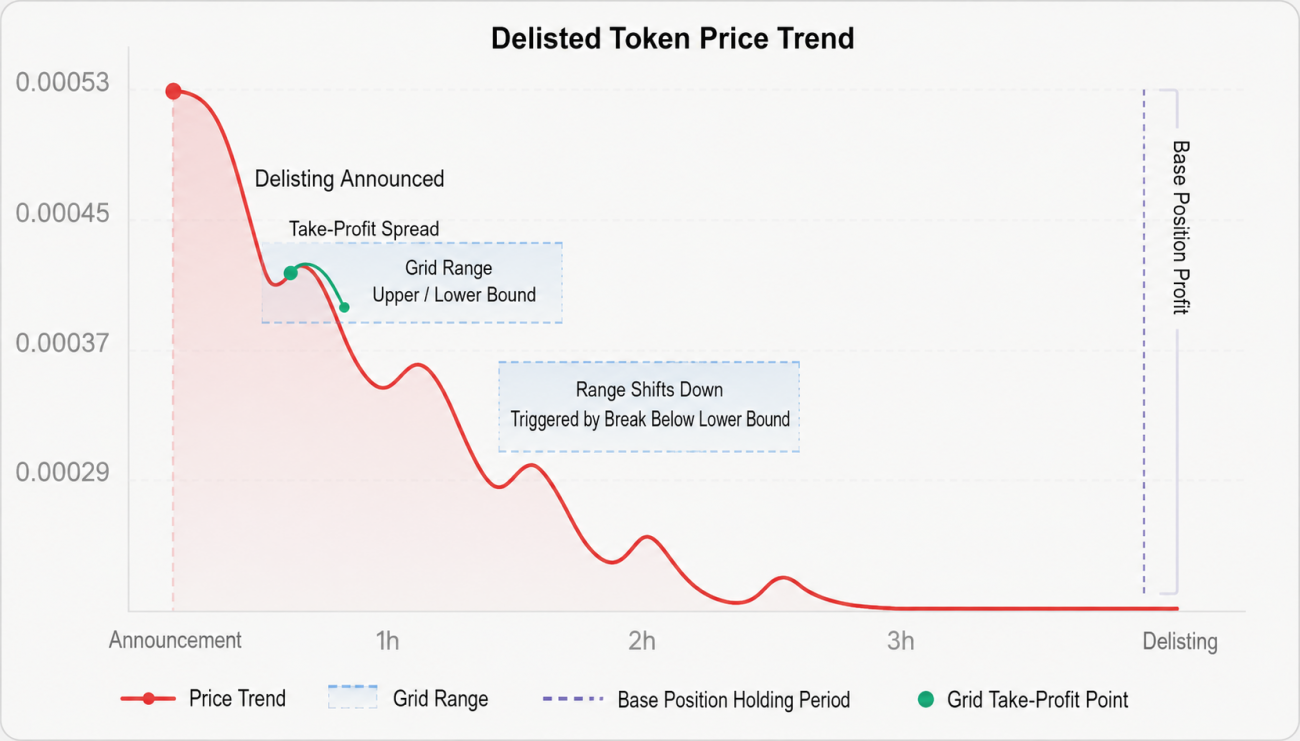

Take the recent MLNUSDT case as an example:

Within half an hour the price lost nearly a third of its value, and the entire delisting cycle typically lasts several days, during which price keeps oscillating at depressed levels. For a short strategy, this is a natural breeding ground.

However, trading these opportunities manually has two real difficulties:

First, the time-sensitivity is extreme. The first 5 minutes after the announcement is the highest-velocity drop window. If you miss the entry, chasing the short later carries significantly more risk. No human can realistically monitor this 24/7.

Second, the move is not a clean one-way waterfall. The price keeps rebounding during the descent. Holding a pure short captures the trend, but you miss out on a large amount of high-frequency mean-reversion profit during those rebounds.

To address both problems, this article presents a complete automated strategy: the program watches Binance for delisting signals in real time, immediately opens a short base position the moment an announcement is detected, simultaneously fires up a dynamic short grid to keep harvesting oscillation profits during the overall downtrend, and automatically closes out before delisting — all without manual intervention.

1. Why This Market Regime Works

Before diving into the strategy, we need to understand the price behavior of delisted tokens — it’s the foundation everything else is built on.

1.1 The Market Shock of a Delisting Announcement

When Binance announces that a perpetual is going to be delisted, the market’s first reaction is panic. Long holders know the contract is about to disappear and must close out before delisting, otherwise they’ll be force-settled. This concentrated selling produces strong short-term sell pressure and drives price down quickly.

At the same time, market makers widen quotes or pull liquidity, which further amplifies the move. This is why the first few minutes after the announcement consistently see the largest drop of the entire delisting cycle.

1.2 The Choppy Downtrend Pattern

After the initial plunge, the price doesn’t drop in a straight line to the bottom. It exhibits a classic choppy downtrend:

There’s an inherent logic to this pattern: each rebound is a short-term trader thinking the drop is overdone and trying to bottom-fish. But the fundamentals haven’t changed (the contract is still about to disappear), so the dip-buyers quickly get trapped and the price resumes its decline. Each rebound is lower than the previous one, until liquidity completely dries up just before delisting.

This kind of structured oscillation is exactly the regime a grid strategy is built for.

1.3 Two Sources of Returns

Based on the analysis above, we can design two independent profit paths:

| Profit Source | Tool | Profitable When |

|---|---|---|

| Trend (downward) | Base short position | Price drops overall |

| Oscillation | Short grid | Price oscillates within a range |

Stacked together, the strategy has solid earning capacity in delisting regimes. Even if a sizable rebound occurs, the grid keeps harvesting spread; and as long as the overall trend is down, the base position keeps producing profit.

2. The Monitoring Principle: How to Detect a Delisting Signal Instantly

For monitoring contract information, this strategy uses a more direct approach: monitor the Binance perpetual API endpoint for data changes directly.

2.1 The Secret of the deliveryDate Field

The Binance fapi/v1/exchangeInfo endpoint returns detailed info on every contract, including a field called deliveryDate — the contract’s settlement time.

For perpetual contracts, this field is normally set to a far-future timestamp:

4133404800000 → corresponds to December 31, 2100

This is effectively a “never expires” placeholder.

The key insight: when Binance decides to delist a perpetual, it updates that contract’s deliveryDate to the actual delisting timestamp at the same moment the announcement is published.

Normal perpetual: deliveryDate = 4133404800000 (never expires)

About-to-delist contract: deliveryDate = 1744106400000 (2026-04-08 17:00:00)

This change is reflected in the API data immediately — faster than the announcement page renders, and in structured form, with no HTML parsing required.

2.2 The Monitoring Code

Poll the endpoint every 15 seconds and filter for USDT perpetuals whose deliveryDate has been switched to a real timestamp:

def fetch_delist_symbols():

body = HttpQuery("https://fapi.binance.com/fapi/v1/exchangeInfo")

data = json.loads(body)

now_ms = get_now_ms()

result = {}

for s in data.get("symbols", []):

if not s["symbol"].endswith("USDT"):

continue

if s.get("contractType") != "PERPETUAL":

continue

dd = s.get("deliveryDate", PERPETUAL_END)

if dd < PERPETUAL_END and dd > now_ms:

result[s["symbol"]] = dd

return result

Sample return value:

{

"HIPPOUSDT": 1744106400000, # 2026-04-08 17:00:00

"OLUSDT": 1744106400000,

"RLSUSDT": 1744106400000,

"PUFFERUSDT": 1744106400000,

}

Note: Live testing shows there is still some latency with this method. You may want to pair it with a faster verification path.

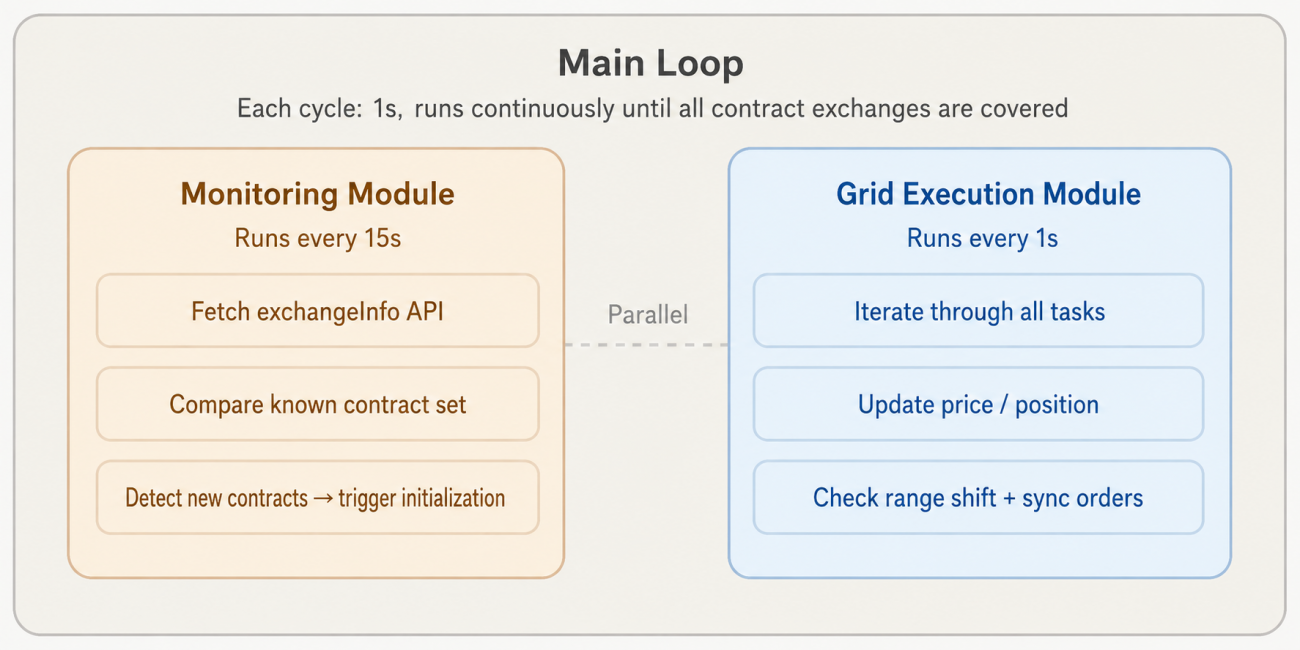

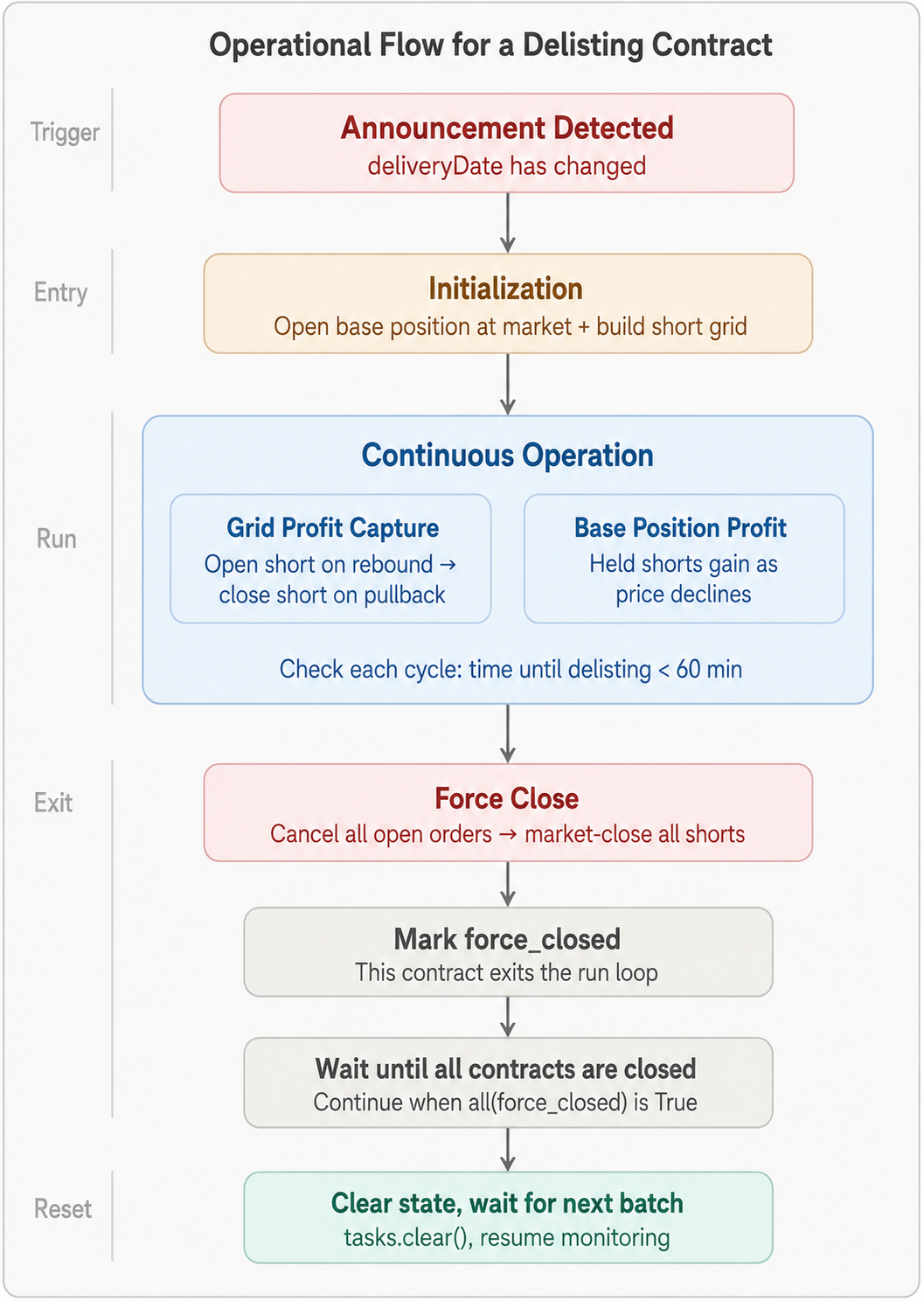

3. Strategy Architecture

The whole system is split into two modules running in parallel:

When a new delisting contract is discovered, a separate task object is created for it, holding all the state for that contract:

task = {

"symbol": "HIPPO_USDT",

"delist_time_ms": 1744106400000,

"fund_per_task": 250.0, # allocated capital

"base_short_qty": 1500000, # base-position size in contracts

"range_high": 0.0005287, # grid upper bound

"range_low": 0.0004758, # grid lower bound

"grid_width": 0.0000529, # range width (fixed)

"grids": [...], # state of 10 grid cells

"shift_count": 0, # number of times the range has shifted

...

}

The task objects for different contracts are fully independent and don’t interfere with each other; they run in parallel.

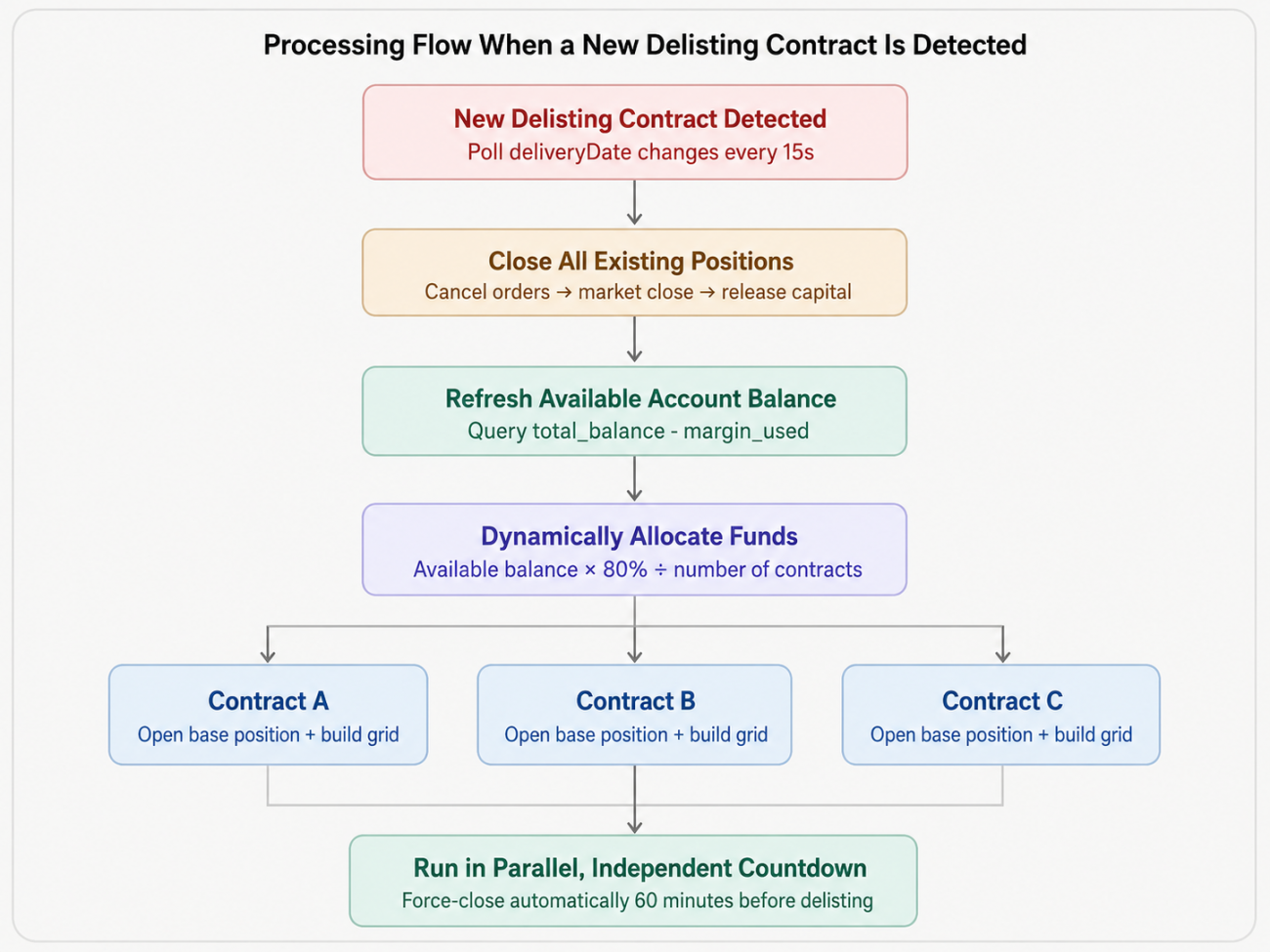

4. Capital Allocation

After discovering N delisting contracts, dynamically split the available balance evenly:

Capital per contract = available balance × 80% / N

20% is reserved as a margin buffer to guard against short-term rebounds triggering liquidation.

Important detail: as multiple contracts are initialized one after another, the available balance shrinks with each initialization (the base position consumes margin). So you can’t compute everyone’s allocation in a single pass before the loop — instead, re-query the balance before each initialization:

for idx, (binance_sym, delist_ms) in enumerate(delist_map.items()):

update_global_account()

remaining_count = total_new - idx

available_now = total_balance - margin_used

fund_per_task = available_now * 0.8 / remaining_count

task = init_task(binance_sym, delist_ms, fund_per_task)

This way every contract gets a reasonable allocation, and you never end up with later contracts starved of capital because earlier ones consumed too much margin.

5. Base Position and Grid in Detail

5.1 Opening the Base Short

The moment the announcement is detected and initialization runs, open a short at market — don’t wait for the grid:

Base notional = allocated capital × 50% × leverage

Example: allocated capital = 250 USDT, leverage = 10x

Base notional = 250 × 50% × 10 = 1,250 USDT

The base position is held throughout, never participating in the grid’s open/close cycles. It’s only closed when the final force-close before delisting kicks in.

The base position is the single biggest profit contributor in the strategy — if a delisted token drops 50% from announcement to delisting, the base position captures that full 50% of short P&L (multiplied by leverage).

5.2 Setting Up the Short Grid

Take the current price as the upper bound, drop 10% below it for the lower bound, and divide into 10 equal grid cells:

Example (current price 0.0005287, range width 10%):

Upper bound = 0.0005287

Lower bound = 0.0005287 × (1 - 10%) = 0.0004758

Cell width = (0.0005287 - 0.0004758) / 10 = 0.0000053

Cell 9: short @ 0.0005287 → cover @ 0.0005234

Cell 8: short @ 0.0005234 → cover @ 0.0005181

Cell 7: short @ 0.0005181 → cover @ 0.0005128

...

Cell 0: short @ 0.0004811 → cover @ 0.0004758

Capital is split equally per cell, and the logic is simple: when price rebounds to the short entry, the sell order fills and a short is opened; when price drops to the cover price, the buy order fills and the short is closed; that completes one round trip, and a new short entry is placed waiting for the next rebound.

5.3 The Order-Placement Strategy at Startup

At startup, every cell whose short entry price is ≥ the current price gets a live order:

Current price: 0.0005287

Cell 9: short entry = 0.0005287 ≥ 0.0005287 → place order ✅

Cell 8: short entry = 0.0005234 < 0.0005287 → skip_below (price has already passed it)

Cell 7 and below: → skip_below

The reason to pre-place every cell above the current price is that, in a downtrend, price can spike up unexpectedly at any moment. Having all of them queued in advance guarantees we don’t miss a short entry on any rebound.

6. Dynamic Range Shifting

This is the most critical mechanism in the whole strategy. Price will not stay forever in the initial range — the grid must move with the price to keep harvesting spread.

6.1 Shifting Down (price breaks below the lower bound)

When price breaks below the grid’s lower bound, the drop has exceeded the current range’s coverage, and the whole range needs to shift down:

Old range: 0.0004758 ~ 0.0005287

Current price: 0.0004500 (broke below 0.0004758)

Compute new range (shift step = 5%):

shift_step = 0.0004500 × 5% = 0.0000225

New upper = 0.0005287 - 0.0000225 = 0.0005062

New lower = 0.0005062 - 0.0000529 = 0.0004533

New range: 0.0004533 ~ 0.0005062

6.2 Shifting Up (rebound exceeds the upper bound)

When the price rebounds above the upper bound, the range shifts up to follow it:

Old range: 0.0004494 ~ 0.0005023

Current price: 0.0005100 (broke above 0.0005023)

Shift the range up so current price falls inside the new range

New range: 0.0004758 ~ 0.0005287

This mechanism guarantees the grid always tracks the price no matter how it moves — you never end up in a situation where price has run away from the range and all the cells sit idle.

6.3 Range Width Stays Constant

Each shift only changes the range’s position, never its width:

grid_width = round(range_high - range_low, 8) # fixed at initialization

# when shifting down

range_high = fp(task, range_high - shift_step)

range_low = fp(task, range_high - grid_width) # compute from fixed width

This prevents floating-point drift from gradually making the range wider or narrower over time.

6.4 Position-Protection Mechanism

When the range shifts, all open orders are canceled and the grid is rebuilt. But what about cells that already have an open short position waiting to be covered?

If you simply rebuild, those positions become “orphaned” — there’s an open short but no corresponding cover order, leaving you with a naked short fully exposed to rebound risk.

The solution: before shifting, sum up the contracts held across all open-short cells; after shifting, place a cover order on the lowest cell of the new range:

# sum up holdings before the shift

holding_contracts = sum(

g.get("sell_contracts", 0)

for g in task["grids"]

if g["status"] in ("pending_cover", "holding_no_cover")

)

cancel_all_orders(task)

activate_grids(task, new_high, new_low)

# after the shift, place a cover-protection order on the lowest cell

if holding_contracts > 0:

_place_grid_cover(task, 0, holding_contracts)

This way, no matter how the range moves, no open short ever loses its cover.

7. Managing Multiple Contracts in Parallel

7.1 Handling Newly Discovered Contracts

Capital released when an old contract finishes its lifecycle re-enters the allocation pool, ensuring new contracts get adequate funding.

7.2 Lifecycle Management

The lifecycle of each contract:

8. A Few Key Details

8.1 The Precision Trap for Small-Price Tokens

For tokens priced in the 0.0003 range like HIPPOUSDT, computing the range shift step hits a precision problem:

shift_step = 0.0003 × 5% = 0.000015

If PricePrecision = 4 (4 decimal places)

round(0.000015, 4) = 0.0 ← step rounds to zero!

→ the while loop never terminates: infinite loop

The fix is to skip the precision truncation on the step, and apply a minimum-step floor:

shift_step = price * SHIFT_STEP_PCT

min_step = 10 ** (-PricePrecision)

shift_step = max(shift_step, min_step) # at least one tick

8.2 Handling a Failed Base-Short Open

The market short can fail due to insufficient funds or a network issue. If it does, you can’t proceed to build the grid — otherwise you’d have a naked grid with no base short underneath it:

def open_base_short(task):

oid = place_market_short(task, usdt_amount)

Sleep(1000)

amt, _, _ = get_short_position(task)

task["base_short_qty"] = amt

if amt <= 0:

Log(f"Base short failed to open, skipping this contract")

return False

return True

# inside init_task

if not open_base_short(task):

return None # initialization failed; don't add to tasks

8.3 Force-Close Timing and Method

The choice of T-60 minutes (rather than T-30 minutes, which is when Binance prohibits new positions) leaves a comfortable time window for closing. The closer you get to delisting, the worse the liquidity, and the harder it becomes to close.

For the close, use a limit order slightly above market rather than a true market order, to avoid getting picked off by predatory matching in low-liquidity conditions:

buy_p = fp(task, price * 1.005) # 0.5% above market

exchange.CreateOrder(swapcode, "closesell", buy_p, fc)

If a close doesn’t fill in one go, retry up to 10 times, refetching the latest price each time.

8.4 Bonus: Funding Rate Revenue

In a downtrend, the funding rate typically favors shorts (shorts get paid). This is extra income for holding the base position — it doesn’t show up in the grid’s spread statistics, but it does show up as growth in account equity.

9. Suggested Parameters

LEVERAGE = 10 # leverage; recommend 5-10, don't go too high

GRID_WIDTH_PCT = 0.10 # 10% range width covers a normal oscillation amplitude

SHIFT_STEP_PCT = 0.05 # 5% shift step, about half the range width

GRID_COUNT = 10 # more cells means less capital per cell

BASE_SHORT_RATIO = 0.5 # 50% base, 40% grid, 10% buffer

FORCE_CLOSE_MINS = 60 # force-close 60 minutes before delisting

MONITOR_INTERVAL = 15000 # poll every 15 seconds; balances responsiveness and rate limits

Choosing the range width: a wider range covers a larger oscillation amplitude, but each cell is also wider apart, so harvest frequency drops. Adjust it based on the historical volatility of the specific token. 10% is a reasonable starting point.

Choosing the cell count: more cells means tighter spacing and higher harvest frequency, but smaller capital and smaller P&L per cell. Too many cells, and the per-cell capital can fall below the exchange’s minimum order size. 10 cells is a balanced choice.

10. Risk Warnings

Before deploying this strategy, you need to be fully aware of the following risks:

Rebound risk: if the news has already been priced in ahead of the announcement, you can get a “sell the news” rebound right after the announcement. The base short will be briefly underwater. The grid will still harvest spread on the rebound, but the strategy can experience a short-term drawdown overall.

Liquidity risk: the closer you get to the delisting time, the worse the contract’s liquidity gets — bid-ask widens, slippage on exit increases. The strategy includes a 0.5% price premium and 10 retries to address this, but under extreme conditions some contracts may still not fully close.

False-signal risk: in rare cases Binance cancels or postpones a delisting. The strategy would continue to hold the short until manual intervention or the next monitoring update overrides it.

High leverage risk: delisted tokens are extremely volatile. At 10x leverage, even a 10% rebound can wipe out close to your full position. Adjust leverage to match your risk tolerance and control overall exposure.

Start/stop in time: live trading reveals that some tokens, after a day of choppy decline, gradually recover to pre-announcement levels. You need to shut the strategy down in time when this happens.

Long runtime: the strategy needs to wait for opportunities — be patient.

11. Summary

The core value of this strategy is converting an information advantage (detecting the delisting signal first) into a trading advantage (automated execution), and using the base + grid dual structure to capture both trend return and oscillation spread in a unidirectional downtrend.

The key design decisions across the system:

| Module | Core Design | Problem It Solves |

|---|---|---|

deliveryDate monitoring | Read the API field directly | Sub-second delisting detection |

| Dynamic capital allocation | Re-query balance before each init | Balanced allocation across contracts |

| Market-order base short | Fire the moment the announcement hits | Don’t miss the first sharp drop |

| Full pre-placement of grid orders | Place every cell above current price | Don’t miss an outsized rebound |

| Fixed range width | Width stays constant on shift | No floating-point drift |

| Position protection | Re-place cover orders after a shift | No naked shorts |

| T-60-minute force-close | Leave enough exit window | Handle low liquidity |

Delisting events don’t happen every day, but every one of them is a relatively high-conviction trading opportunity. With programmatic monitoring and execution, you can participate in these opportunities steadily — without staring at the screen.