Strategy Name: Relative Strength Strategy Based on Price

Data cycle: 1H

Support: Commodity Futures, Digital Currency and Digital Currency Futures

- Main chart:

MA, formula: MAN^^MA(C,N); - Secondary chart:

none

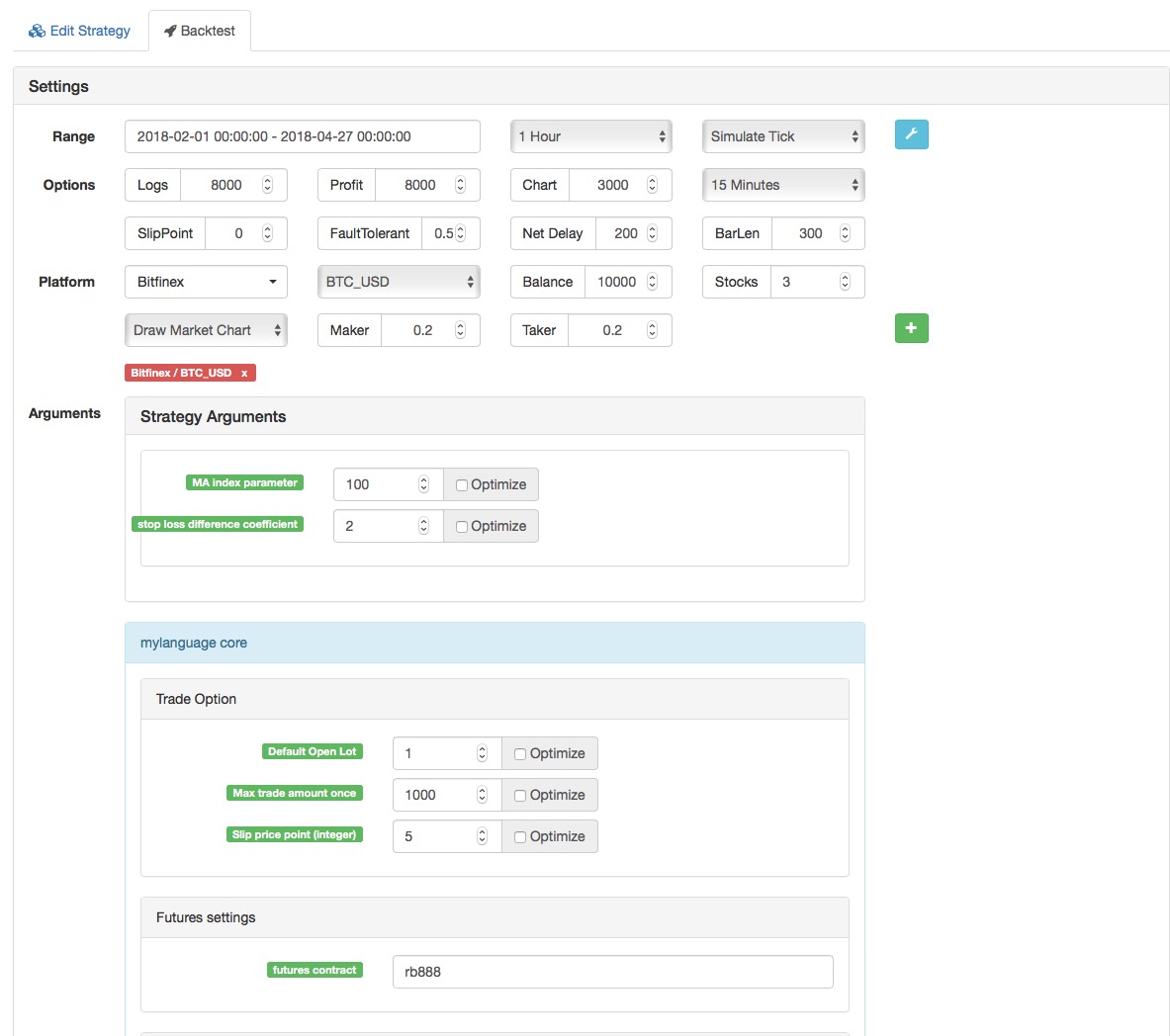

(*backtest

start: 2018-02-01 00:00:00

end: 2018-04-27 00:00:00

period: 1h

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

args: [["ContractType","rb888",126961]]

*)

MAN^^MA(C,N);

B_MA:=C>MAN;

S_MA:=C<MAN;

S_K1:=SUM((H-C)*V,N)/SUM((H-L)*V,N)>0.5;

B_K1:=SUM((C-L)*V,N)/SUM((H-L)*V,N)>0.5;

CO:=IF(C>O,C-O,0);

OC:=IF(C<O,O-C,0);

S_K2:=SUM(OC*V,N)/SUM(ABS(C-O)*V,N)>0.5;

B_K2:=SUM(CO*V,N)/SUM(ABS(C-O)*V,N)>0.5;

B_K1 AND B_K2 AND B_MA AND H>=HHV(H,N),BPK;

S_K1 AND S_K2 AND S_MA AND L<=LLV(L,N),SPK;

STOPLOSS:=M*MA(H-L,N);

C<BKPRICE-STOPLOSS,SP(BKVOL);

C>SKPRICE+STOPLOSS,BP(SKVOL);

S_MA AND BKHIGH>BKPRICE+STOPLOSS,SP(BKVOL);

B_MA AND SKLOW<SKPRICE-STOPLOSS,BP(SKVOL);

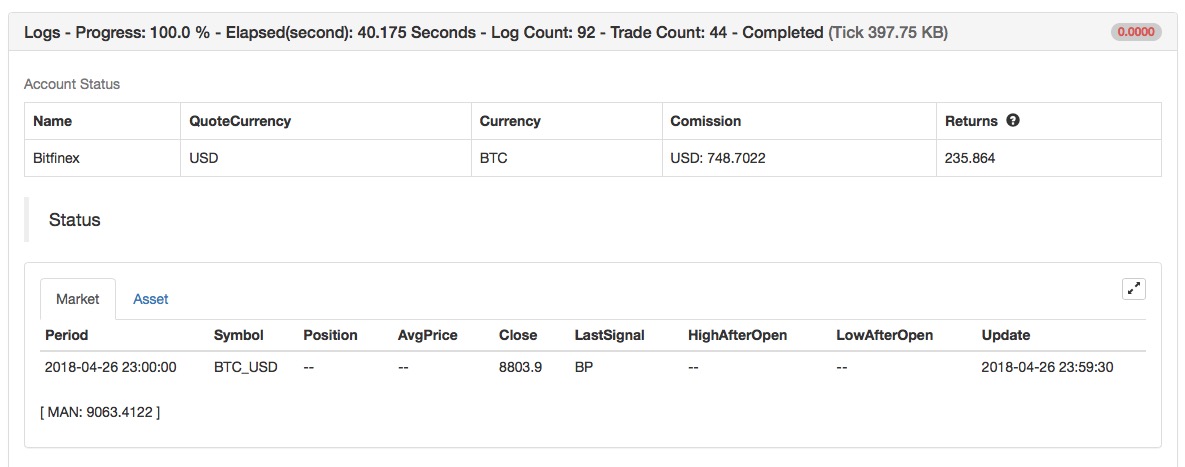

Backtest on FMZ Quant to know more

Source Code: https://www.fmz.com/strategy/129078