When writing and using strategies, we often use some rarely used K-line period data. However, exchanges and data sources do not provide data on these periods. It can only be synthesized by using data with an existing period. The synthesized algorithm already has a JavaScript version (link). In fact, it is easy to transplant a piece of JavaScript code to Python. Next, let’s write a Python version of the K-line synthesis algorithm.

JavaScript version

function GetNewCycleRecords (sourceRecords, targetCycle) { // K-line synthesis function

var ret = []

// Obtain the period of the source K-line data first

if (!sourceRecords || sourceRecords.length < 2) {

return null

}

var sourceLen = sourceRecords.length

var sourceCycle = sourceRecords[sourceLen - 1].Time - sourceRecords[sourceLen - 2].Time

if (targetCycle % sourceCycle != 0) {

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

throw "targetCycle is not an integral multiple of sourceCycle."

}

if ((1000 * 60 * 60) % targetCycle != 0 && (1000 * 60 * 60 * 24) % targetCycle != 0) {

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

Log((1000 * 60 * 60) % targetCycle, (1000 * 60 * 60 * 24) % targetCycle)

throw "targetCycle cannot complete the cycle."

}

var multiple = targetCycle / sourceCycle

var isBegin = false

var count = 0

var high = 0

var low = 0

var open = 0

var close = 0

var time = 0

var vol = 0

for (var i = 0 ; i < sourceLen ; i++) {

// Get the time zone offset value

var d = new Date()

var n = d.getTimezoneOffset()

if (((1000 * 60 * 60 * 24) - sourceRecords[i].Time % (1000 * 60 * 60 * 24) + (n * 1000 * 60)) % targetCycle == 0) {

isBegin = true

}

if (isBegin) {

if (count == 0) {

high = sourceRecords[i].High

low = sourceRecords[i].Low

open = sourceRecords[i].Open

close = sourceRecords[i].Close

time = sourceRecords[i].Time

vol = sourceRecords[i].Volume

count++

} else if (count < multiple) {

high = Math.max(high, sourceRecords[i].High)

low = Math.min(low, sourceRecords[i].Low)

close = sourceRecords[i].Close

vol += sourceRecords[i].Volume

count++

}

if (count == multiple || i == sourceLen - 1) {

ret.push({

High : high,

Low : low,

Open : open,

Close : close,

Time : time,

Volume : vol,

})

count = 0

}

}

}

return ret

}

There are JavaScript algorithms. Python can be translated and transplanted line by line. If you encounter JavaScript built-in functions or inherent methods, you can go to Python to find the corresponding methods. Therefore, the migration is easy.

The algorithm logic is exactly the same, except that JavaScript function calls var n=d.getTimezoneOffset(). When migrating to Python,n=time.altzone in Python’s time library is used instead. Other differences are only in terms of language grammar (such as the use of for loops, Boolean values, logical AND, logical NOT, logical OR, etc.).

Migrated Python code:

import time

def GetNewCycleRecords(sourceRecords, targetCycle):

ret = []

# Obtain the period of the source K-line data first

if not sourceRecords or len(sourceRecords) < 2 :

return None

sourceLen = len(sourceRecords)

sourceCycle = sourceRecords[-1]["Time"] - sourceRecords[-2]["Time"]

if targetCycle % sourceCycle != 0 :

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

raise "targetCycle is not an integral multiple of sourceCycle."

if (1000 * 60 * 60) % targetCycle != 0 and (1000 * 60 * 60 * 24) % targetCycle != 0 :

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

Log((1000 * 60 * 60) % targetCycle, (1000 * 60 * 60 * 24) % targetCycle)

raise "targetCycle cannot complete the cycle."

multiple = targetCycle / sourceCycle

isBegin = False

count = 0

barHigh = 0

barLow = 0

barOpen = 0

barClose = 0

barTime = 0

barVol = 0

for i in range(sourceLen) :

# Get the time zone offset value

n = time.altzone

if ((1000 * 60 * 60 * 24) - (sourceRecords[i]["Time"] * 1000) % (1000 * 60 * 60 * 24) + (n * 1000)) % targetCycle == 0 :

isBegin = True

if isBegin :

if count == 0 :

barHigh = sourceRecords[i]["High"]

barLow = sourceRecords[i]["Low"]

barOpen = sourceRecords[i]["Open"]

barClose = sourceRecords[i]["Close"]

barTime = sourceRecords[i]["Time"]

barVol = sourceRecords[i]["Volume"]

count += 1

elif count < multiple :

barHigh = max(barHigh, sourceRecords[i]["High"])

barLow = min(barLow, sourceRecords[i]["Low"])

barClose = sourceRecords[i]["Close"]

barVol += sourceRecords[i]["Volume"]

count += 1

if count == multiple or i == sourceLen - 1 :

ret.append({

"High" : barHigh,

"Low" : barLow,

"Open" : barOpen,

"Close" : barClose,

"Time" : barTime,

"Volume" : barVol,

})

count = 0

return ret

# Test

def main():

while True:

r = exchange.GetRecords()

r2 = GetNewCycleRecords(r, 1000 * 60 * 60 * 4)

ext.PlotRecords(r2, "r2")

Sleep(1000)

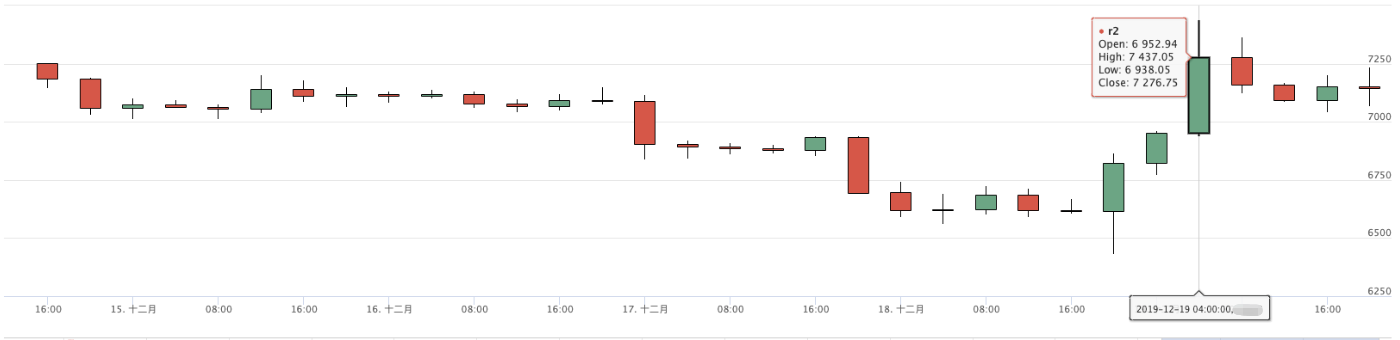

Test

Huobi market chart

4-hour chart of backtest synthesis

The above code is for reference only. If it is used in specific strategies, please modify and test according to the specific requirements.

If there is a bug or improvement suggestion, please leave a message. Thank you very much. o^_^ o