www.fmz.com Summary For the development of quantitative trading strategies, the first thing to do is the configuration of the trading tools. In this section we will take you through setting up exchang...

www.fmz.com Summary In the previous chapter, we learned about the concepts of quantitative trading, have a basic understanding of quantitative trading. So what tools are available on the market that c...

Summary A complete strategy is actually a set of rules that traders give themselves. It includes all aspects of the trading, and does not leave a little room for subjective imagination. Every choices ...

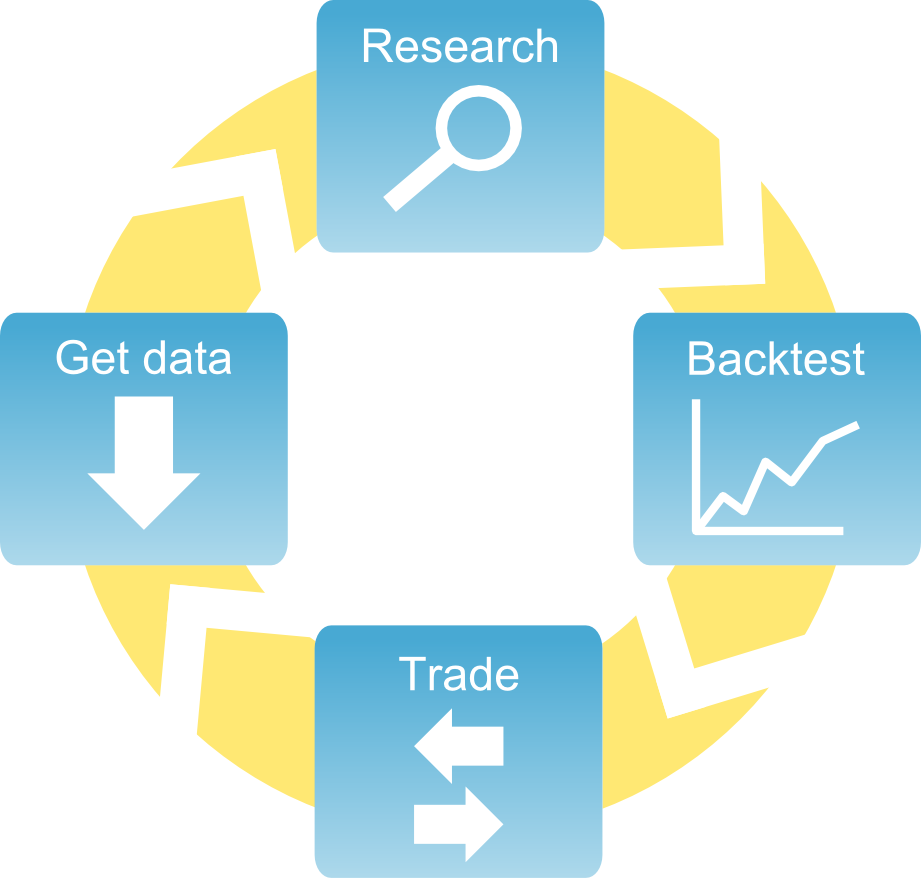

Summary A complete quantitative trading life cycle is more than just the trading strategy itself. It consists of at least six parts, including: strategy design, model building, backtesting tuning, sim...

Summary Many people think complex trading strategies as a starting point when discussing quantitative trading, and inadvertently put a layer of mystery on quantitative trading. In this section, we wil...

Summary As a product of the combination of science and machine, quantitative trading is changing the pattern of modern financial markets. Many investors have turned their attention to this field. How ...

Quantitative trading quick start Content Part 1, the basis of quantitative trading What is quantitative trading? Why choose quantitative trading? What are the needs for quantitative trading? What are ...

article originally from : https://www.quandl.com/ MACD is a popularly used technical indicator in trading stocks, currencies, cryptocurrencies, etc. Basics of MACD MACD is used and discussed in many d...

When going for an automated trading platform it is very important to look for some important features before you decide on the automated trading platform you want to trade on. Different auto...

We have a large number of vendor-developed backtesting platforms available in the market which can be very efficient in backtesting automated strategies, but to decide which ones will suit your r...