Place order after K line is done, open or close position when closing price is determined

Data Level: Daily K Line

- Main chart:

MIDTR^^MA(C,CN); // Determine MIDTR

UPTR^^MIDTR+2STD(C,CN); // Determine UPTR

DOWNTR^^MIDTR-2STD(C,CN); // Determine DOWNTR

HPOINT^^HV(H,CN), DOT, COLORRED;

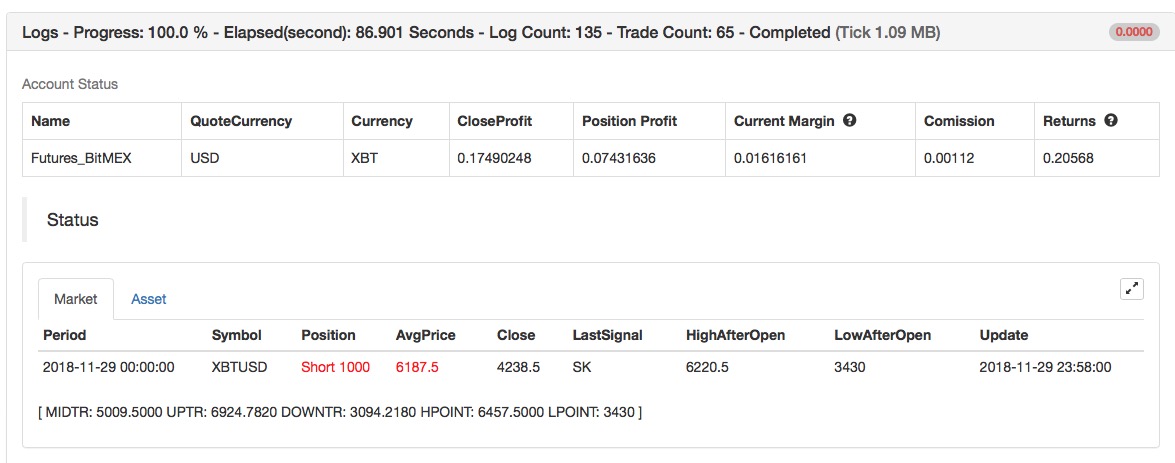

// Calculate the maximum value of the highest price in the CN cycle of the previous cycle.

LPOINT^^LV(L,CN), DOT, COLORBLUE;

// Calculate the minimum value of the lowest price in the CN cycle of the previous cycle. - Secondary chart:

none

(*backtest

start: 2017-07-01 00:00:00

end: 2018-11-30 00:00:00

period: 1d

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

*)

// Determine CN

VOLAT:=STD(C,N); // VOLAT(volatility): Standard deviation of closing price in M-cycle

VOLATCHANGE:=(VOLAT-REF(VOLAT,1))/VOLAT; // Change rate of two VOLATs

N1:=(1+VOLATCHANGE)*MINN; // VOLATCHANGE : Volatility change

N2:=INTPART(N1); // Rounding off an integer

N3:=MIN(N2,MAXN); // Confirm that CN is no more than 60

CN:=MAX(N3,MINN); // Confirm that CN is no less than 20

MIDTR^^MA(C,CN); // Determine MIDTR

UPTR^^MIDTR+2*STD(C,CN); // Determine UPTR

DOWNTR^^MIDTR-2*STD(C,CN); // Determine DOWNTR

HPOINT^^HV(H,CN),DOT,COLORRED; // see main chart

LPOINT^^LV(L,CN),DOT,COLORBLUE; // see main chart

// open position

L<=LPOINT AND L<DOWNTR AND BARPOS>MINN,SK(AMOUNT);

// when the lowest price < the lowest point and DOWNTR

and the K-line position > 60, sell short the closing price

H>=HPOINT AND H>UPTR AND BARPOS>MINN,BK(AMOUNT);

// when the highest price > UPTR and the highest point,

and the K-line position > 60, buy long the closing price

// start stop loss

C>=SKPRICE*(1+STOPRANGE*0.001),BP(SKVOL);

C<=BKPRICE*(1-STOPRANGE*0.001),SP(BKVOL);

// close position

C<MIDTR,SP(BKVOL); // when closing price < MIDTR, sell the closing price

C>MIDTR,BP(SKVOL); // when closing price > MIDTR, buy to cover the closing price

// Dynamic stop loss

REF(BKHIGH,1)>BKPRICE*(1+2*0.001*STOPRANGE) AND C<HV(C,BARSBK)*(1-STOPRANGE*0.001),SP(BKVOL);

// the highest price after buying long > buy long price*(1+2*0.001*STOPRANGE),

and closing price < the highest closing price after buying long*(1-STOPRANGE*0.001),

then sell closing price.

REF(SKLOW,1)<SKPRICE*(1-2*0.001*STOPRANGE) AND C>LV(C,BARSSK)*(1+STOPRANGE*0.001),BP(SKVOL);

// the lowest price after sellong short < sell short price *(1-2*0.001*STOPRANGE),

and closing price > the lowest closing price after selling short*(1+STOPRANGE*0.001),

then buy to cover closing price.

Backtest on FMZ Quant to know more

Source Code: https://www.fmz.com/strategy/128129